Concerns over the Wuhan Coronavirus (WCV) pandemic will dominate investor thinking, as the infection rate climbs with sentiment dictated by news flow. The re-opening of stock markets in China next Monday following the extended Lunar New Year closure will not be for the faint-hearted. The WCV is hardly the first global health scare, and our base case expectation is for the spread to be successfully contained in the months ahead. The ensuing market volatility will present opportunities to accumulate.

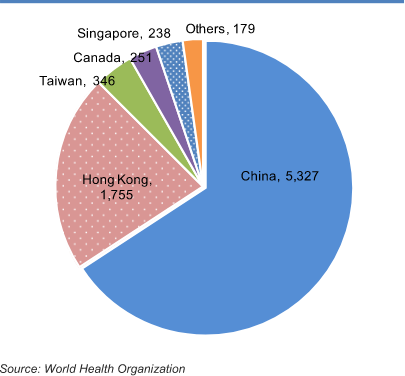

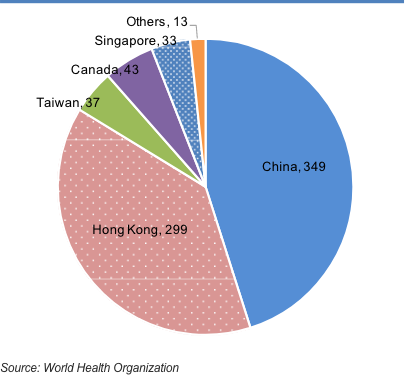

Largely contained within China.

The data shows that infections remain largely contained within China, while

those infected outside China are either Chinese nationals or those that had

travelled to Wuhan/Hubei. An escalation of

person-to-person infections of people outside China would be a major concern.

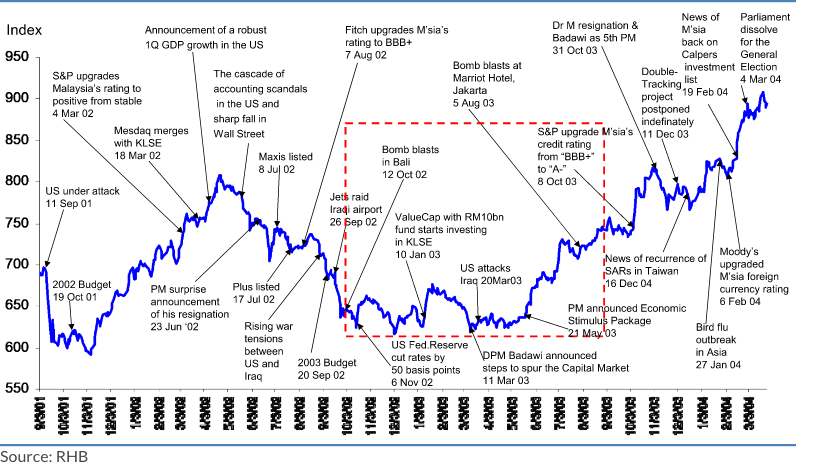

SARS (Nov 2002-Jul 2003) comparisons.

Much has been made of the seemingly faster rate of WCV infections compared to

SARS, where the number of infected persons reached 9,160 in just three weeks

(SARS: 8,069 case over the entire

outbreak). However, we note that SARS data could have been under-reported, due

to the Chinese government’s attempts to suppress information. It is also

difficult to discern the direct impact of

SARS on the market during that period due to ongoing geopolitical events at that

time, which included the US invasion of Iraq, Bali and Jakarta bombings, as well

as other domestic political

developments (Figure 1).

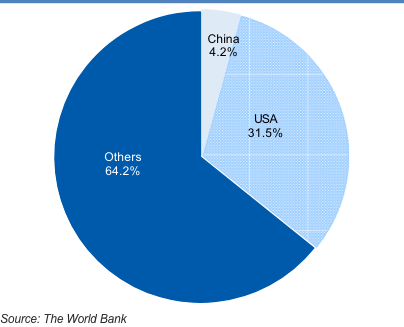

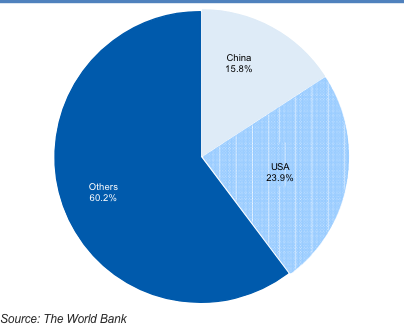

China is now a big player.

A key risk is the possible second round effect on markets from an economic slowdown in

China, if the WCV pandemic remains unresolved – especially as the global growth cycle is

already at a matured stage.

China is now the world’s second largest economy, accounting for 16% of global GDP (from

4% in 2002) with extensive trade links and connectivity. The impact on China’s economy

should be mitigated by

expected stimulus measures. We are also reassured on the progress to finding a cure with

the sequencing of the virus’ genome available on 10 Jan, a month after the first case

was reported (SARS genome was

sequenced in Apr 2003).

Market technicals.

Market trends remain decidedly bearish, with a “Double Top” pattern forming and the FBM

KLCI is currently in the key support zone between 1,500-1,550 pts. A breakdown below

this should see the next

support at 1,300 pts, while the upside resistance is at 1,600 pts.

A second bite of the cherry.

The worst-case scenario is that this WCV pandemic could tip the world into a recession –

which is a remote possibility, at this juncture. The Ministry of Finance also stands

ready to implement a domestic

stimulus package. Consistent with our existing trading market strategy to accumulate on

dips, persistently negative market sentiment and weakness should be viewed as

opportunities.

Sector: Auto

Impact: Neutral

Comment: It should have a minimal direct impact on the local automotive

industry. However, if the local situation is exacerbated, industry sales will be

negatively impacted as consumers may hold

back on discretionary spending. The impact will be negative on Sime Darby, as it

has significant operational exposure to China. If the situation is prolonged,

there could be a supply chain

disruption risk to Proton as the X70 CKD kit is sourced from China.

Sector: Aviation

Impact: Negative

Comment: We expect travel demand to decline due to fear of the WCV spreading.

Besides that, precautionary measures have caused AirAsia and Malindo Air to

suspend flights to Wuhan.

Sector: Banks

Impact: Negative

Comment: Concerns over a potential slowdown in China’s economic growth will

weigh on business sentiment while measures taken to contain the spread of the

virus will also dampen business

activities. We expect loan growth to remain subdued in 1Q20, with prospects of a

pick-up in 2H20 still intact – if the outbreak is contained by 2Q20. The

possibility of another OPR cut to support

GDP growth will pose a downside risk to earnings.

Sector: Basic Materials

Impact: Neutral

Comment: Aluminium prices (in tandem with that of other base metals) have eased,

on fears of lower demand – with China accounting for over half of global

consumption. However, this would be

potentially mitigated by supply disruptions as well as lower alumina raw

material prices

Sector: Construction

Impact: Neutral

Comment: The travel restriction on Chinese workers presents a downside risk, but

it looks muted for now. While this creates a delay for workers reporting to

work, the impact of a labour shortage

is likely temporary and mostly manageable. New recruits could always be sourced

from existing pipelines, which we understand is always high in supply.

Sector: Consumer

Impact: Negative

Comment: If the situation is prolonged, and/or there are cases of locals being

infected, we will likely to see a reduction in tourist arrivals and locals would

also opt to stay home. This could

all lead to lower footfalls to retail stores. Taking into account the fixed

operating costs and lower volume, profitability will be under pressure for

retail-based businesses. The stocks under our

coverage that could be affected include AEON, Padini, Mynews and Berjaya Food.

Sector: Gaming

Impact: Negative

Comment: Earnings for Genting Malaysia and Genting would be negatively impacted,

as visitor arrivals should decline. During the peak of the SARS pandemic, GenM’s

2Q03 PBT for the leisure &

hospitality segment declined 24% YoY. However, FY03 only declined by 3% as 2H

earnings came in stronger after the pandemic stabilised. Similarly, its share

price quickly rebounded within 1-2

months after both GenM and GenT posted declines of 22% and 23% respectively from

February to April 2003.

Sector: Healthcare

Impact: Positive

Comment: The fear of the WCV spreading bodes well for this sector, as it implies

increased demand for healthcare services. Pharmaceutical companies should also

benefit, as the greater need to

boost immune systems will lead to an increased demand for vitamins.

Sector: Logistics

Impact: Neutral

Comment: Supply chain disruptions affecting the movement of goods in and out of

China could present some uncertainty on ports, courier volumes as well as

shipping costs. However this is expected

to be short-lived.

Sector: Media

Impact: Neutral

Comment: Minimal impact on media companies in general, as the structural issues

afflicting the sector have bigger implications. There is a downside risk to adex

if the pandemic prolongs, with

Visit Malaysia Year (VMY 2020) being a key adex event.

Sector: Non-Bank Financials

Impact: Neutral

Comment: No direct impact from the pandemic. If the situation is prolonged, and

this slows down economic growth, it may dampen demand for general insurance

products.

Sector: Oil & Gas

Impact: Neutral

Comment: We do not expect crude prices to react in a similar pattern as compared

to the SARS outbreak back in 2003, where crude oil prices retraced >30% from

mid-USD30s to mid-USD20s – because

prices were also largely driven by events related to the US’ invasion of Iraq.

Overall, we believe the impact on the sector is rather neutral unless there is a

significant slowdown is China’s

crude oil consumption.

Sector: Plantations

Impact: Neutral

Comment: As palm oil is a basic food staple, demand should not be affected, as

was the case during the SARS breakout. During the SARS breakout, CPO exports to

China from Malaysia actually rose 38%

YoY in 2003 and again by 10.5% in 2004. Demand for Malaysian palm oil from China

of 2.5m tonnes in 2003 is similar to the volume China imported in 2019.

Sector: Property

Impact: Neutral

Comment: The property market is very much domestically-driven and, given the

clampdown on speculative buying since 2014, the number of foreign buyers has

decreased significantly. However, the

outbreak will nonetheless sparks market concerns on economic growth, so

sentiment on the property market may be dampened again.

Sector: REITs

Impact: Neutral

Comment: Minimal impact, but retail REITs with a significant presence in the

city centre are likely to be under pressure, ie KLCCP Stapled, Pavilion REIT as

their prime retail assets (Suria KLCC,

Pavilion Mall Kuala Lumpur) count as tourist attractions. A prolonged outbreak

may affect the bottomline, so we will monitor the health crisis closely. For

now, the REITs sector is still a safe

haven given its defensive nature, especially during times of economic

uncertainty.

Sector: Rubber products

Impact: Positive

Comment: The fear of the outbreak bodes well for rubber glove makers – as demand

for rubber gloves spikes up. Beyond this increase in the near term, we expect

health awareness to rise faster –

which is positive for long-term demand growth.

Sector: Tech

Impact: Neutral

Comment: No significant direct impact. However, should the pandemic outbreak

taking longer to contain, it could affect the sector negatively due to the

disruption in supply chain and/or weak

consumer spending.

Sector: Telecoms

Impact: Neutral

Comment: Minimal impact, with possibly some (short-lived) weakness in roaming

revenues. Rising risk aversion would be positive on high-yield telcos such as

Digi.Com.

Sector: Utilities

Impact: Neutral

Comment: We believe the event will not materially impact overall domestic

electricity demand, and IPP earnings are likely to be unaffected. All in, we are

keeping our electricity demand growth

assumption at 2-3%in 2020 (vs 9M19’s 3.2%) in view of slower economic

activities.

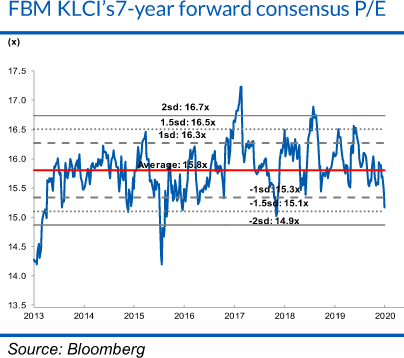

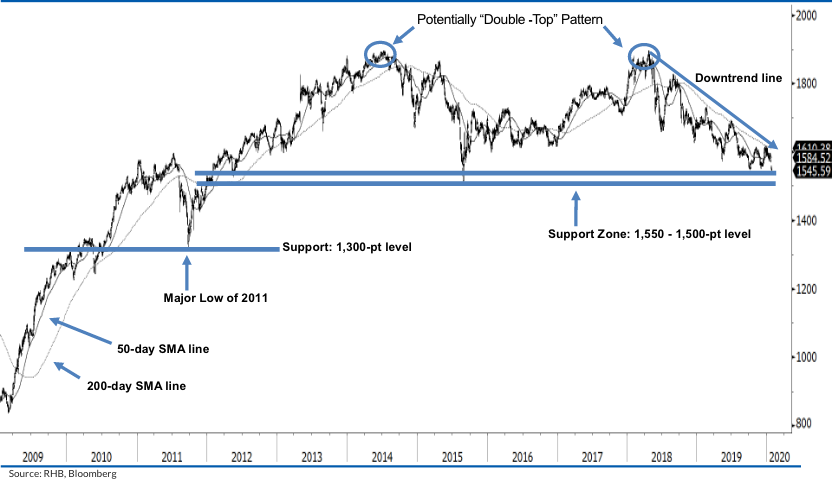

Currently, we deem the FBM KLCI’s trend as bearish, as the index is still trading below the downtrend line. The aforementioned downtrend line comprises the highest points of Apr 2018, Aug 2018 and Jul 2019. In addition, it remains below the declining medium-term 50-day and long-term 200-day SMA lines – which means that the negatives have been enhanced.

Eyeing the key support zone of 1,550 pts to 1,500 pts. This support zone, which is determined from the psychological spot and is also near the lowest point of 2015, can now be used as a strong support level. Should the key support zone be taken out decisively, we expect the downward momentum to continue. The next support is at 1,300 pts, obtained from the major low in 2011.

Potential “Double Top” pattern. We also notice a downside development in the form of a bearish reversal sign, following the “Double Top” pattern. However, a decisive breakdown from the 1,500-pt threshold is needed to validate the further market retracement.

Towards the upside. The immediate resistance level is at the 1,600-pt round figure, near the downtrend line and above the 200-day SMA line. If this level is taken out, the next resistance will likely be at 1,695 pts, ie near the high of 2 Jul 2019.

Buy: Share price may exceed 10% over the next 12 months

Trading Buy: Share price may exceed 15% over the next 3 months, however

longer-term outlook remains uncertain

Neutral: Share price may fall within the range of +/- 10% over the next

12 months

Take Profit: Target price has been attained. Look to accumulate at

lower levels

Sell: Share price may fall by more than 10% over the next 12 months

Not Rated: Stock is not within regular research coverage

Investment Research Disclaimers

RHB has issued this report for information purposes only. This report is intended for

circulation amongst RHB and its affiliates’ clients generally or such persons as may be

deemed eligible by RHB to

receive this report and does not have regard to the specific investment objectives,

financial situation and the particular needs of any specific person who may receive this

report. This report is not

intended, and should not under any circumstances be construed as, an offer or a

solicitation of an offer to buy or sell the securities referred to herein or any related

financial instruments.

This report may further consist of, whether in whole or in part, summaries, research, compilations, extracts or analysis that has been prepared by RHB’s strategic, joint venture and/or business partners. No representation or warranty (express or implied) is given as to the accuracy or completeness of such information and accordingly investors should make their own informed decisions before relying on the same.

This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to the applicable laws or regulations. By accepting this report, the recipient hereof (i) represents and warrants that it is lawfully able to receive this document under the laws and regulations of the jurisdiction in which it is located or other applicable laws and (ii) acknowledges and agrees to be bound by the limitations contained herein. Any failure to comply with these limitations may constitute a violation of applicable laws.

All the information contained herein is based upon publicly available information and has been obtained from sources that RHB believes to be reliable and correct at the time of issue of this report. However, such sources have not been independently verified by RHB and/or its affiliates and this report does not purport to contain all information that a prospective investor may require. The opinions expressed herein are RHB’s present opinions only and are subject to change without prior notice. RHB is not under any obligation to update or keep current the information and opinions expressed herein or to provide the recipient with access to any additional information. Consequently, RHB does not guarantee, represent or warrant, expressly or impliedly, as to the adequacy, accuracy, reliability, fairness or completeness of the information and opinion contained in this report. Neither RHB (including its officers, directors, associates, connected parties, and/or employees) nor does any of its agents accept any liability for any direct, indirect or consequential losses, loss of profits and/or damages that may arise from the use or reliance of this research report and/or further communications given in relation to this report. Any such responsibility or liability is hereby expressly disclaimed.

Whilst every effort is made to ensure that statement of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable and must not be construed as a representation that the matters referred to therein will occur. Different assumptions by RHB or any other source may yield substantially different results and recommendations contained on one type of research product may differ from recommendations contained in other types of research. The performance of currencies may affect the value of, or income from, the securities or any other financial instruments referenced in this report. Holders of depositary receipts backed by the securities discussed in this report assume currency risk. Past performance is not a guide to future performance. Income from investments may fluctuate. The price or value of the investments to which this report relates, either directly or indirectly, may fall or rise against the interest of investors.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

This report may contain forward-looking statements which are often but not always identified by the use of words such as “believe”, “estimate”, “intend” and “expect” and statements that an event or result “may”, “will” or “might” occur or be achieved and other similar expressions. Such forward-looking statements are based on assumptions made and information currently available to RHB and are subject to known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievement to be materially different from any future results, performance or achievement, expressed or implied by such forward-looking statements. Caution should be taken with respect to such statements and recipients of this report should not place undue reliance on any such forward-looking statements. RHB expressly disclaims any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or circumstances after the date of this publication or to reflect the occurrence of unanticipated events.

The use of any website to access this report electronically is done at the recipient’s own risk, and it is the recipient’s sole responsibility to take precautions to ensure that it is free from viruses or other items of a destructive nature. This report may also provide the addresses of, or contain hyperlinks to, websites. RHB takes no responsibility for the content contained therein. Such addresses or hyperlinks (including addresses or hyperlinks to RHB own website material) are provided solely for the recipient’s convenience. The information and the content of the linked site do not in any way form part of this report. Accessing such website or following such link through the report or RHB website shall be at the recipient’s own risk.

This report may contain information obtained from third parties. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. Third party content providers give no express or implied warranties, including, but not limited to, any warranties of merchantability or fitness for a particular purpose or use. Third party content providers shall not be liable for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including lost income or profits and opportunity costs) in connection with any use of their content.

The research analysts responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his or her personal views and opinions about any and all of the issuers or securities analysed in this report and were prepared independently and autonomously. The research analysts that authored this report are precluded by RHB in all circumstances from trading in the securities or other financial instruments referenced in the report, or from having an interest in the company(ies) that they cover.

The contents of this report is strictly confidential and may not be copied, reproduced, published, distributed, transmitted or passed, in whole or in part, to any other person without the prior express written consent of RHB and/or its affiliates. This report has been delivered to RHB and its affiliates’ clients for information purposes only and upon the express understanding that such parties will use it only for the purposes set forth above. By electing to view or accepting a copy of this report, the recipients have agreed that they will not print, copy, videotape, record, hyperlink, download, or otherwise attempt to reproduce or re-transmit (in any form including hard copy or electronic distribution format) the contents of this report. RHB and/or its affiliates accepts no liability whatsoever for the actions of third parties in this respect.

The contents of this report are subject to copyright. Please refer to Restrictions on Distribution below for information regarding the distributors of this report. Recipients must not reproduce or disseminate any content or findings of this report without the express permission of RHB and the distributors.

The securities mentioned in this publication may not be eligible for sale in some states or countries or certain categories of investors. The recipient of this report should have regard to the laws of the recipient’s place of domicile when contemplating transactions in the securities or other financial instruments referred to herein. The securities discussed in this report may not have been registered in such jurisdiction. Without prejudice to the foregoing, the recipient is to note that additional disclaimers, warnings or qualifications may apply based on geographical location of the person or entity receiving this report.

The term “RHB” shall denote, where appropriate, the relevant entity distributing or disseminating the report in the particular jurisdiction referenced below, or, in every other case, RHB Investment Bank Berhad and its affiliates, subsidiaries and related companies.

Malaysia

This report is issued and distributed in Malaysia by RHB Investment Bank Berhad

(“RHBIB”). The views and opinions in this report are our own as of the date hereof and

is subject to change. If the

Financial Services and Markets Act of the United Kingdom or the rules of the Financial

Conduct Authority apply to a recipient, our obligations owed to such recipient therein

are unaffected. RHBIB has no

obligation to update its opinion or the information in this report.

Thailand

This report is issued and distributed in the Kingdom of Thailand by RHB Securities

(Thailand) PCL, a licensed securities company that is authorised by the Ministry of

Finance, regulated by the Securities

and Exchange Commission of Thailand and is a member of the Stock Exchange of Thailand.

The Thai Institute of Directors Association has disclosed the Corporate Governance

Report of Thai Listed Companies

made pursuant to the policy of the Securities and Exchange Commission of Thailand. RHB

Securities (Thailand) PCL does not endorse, confirm nor certify the result of the

Corporate Governance Report of Thai

Listed Companies

Indonesia

This report is issued and distributed in Indonesia by PT RHB Sekuritas Indonesia. This

research does not constitute an offering document and it should not be construed as an

offer of securities in

Indonesia. Any securities offered or sold, directly or indirectly, in Indonesia or to

any Indonesian citizen or corporation (wherever located) or to any Indonesian resident

in a manner which constitutes a

public offering under Indonesian laws and regulations must comply with the prevailing

Indonesian laws and regulations.

Singapore

This report is issued and distributed in Singapore by RHB Securities Singapore Pte Ltd

which is a holder of a capital markets services licence and an exempt financial adviser

regulated by the Monetary

Authority of Singapore. RHB Securities Singapore Pte Ltd may distribute reports produced

by its respective foreign entities, affiliates or other foreign research houses pursuant

to an arrangement under

Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in

Singapore to a person who is not an Accredited Investor, Expert Investor or an

Institutional Investor, RHB

Securities Singapore Pte Ltd accepts legal responsibility for the contents of the report

to such persons only to the extent required by law. Singapore recipients should contact

RHB Securities Singapore

Pte Ltd in respect of any matter arising from or in connection with the report.

Hong Kong

This report is issued and distributed in Hong Kong by RHB Securities Hong Kong Limited

(興業僑豐證券有限公司) (CE No.: ADU220) (“RHBSHK”) which is licensed in Hong Kong by the

Securities and Futures

Commission for Type 1 (dealing in securities) and Type 4 (advising on securities)

regulated activities. Any investors wishing to purchase or otherwise deal in the

securities covered in this report should

contact RHBSHK. RHBSHK is a wholly owned subsidiary of RHB Hong Kong Limited; for the

purposes of disclosure under the Hong Kong jurisdiction herein, please note that RHB

Hong Kong Limited with its

affiliates (including but not limited to RHBSHK) will collectively be referred to as

“RHBHK.” RHBHK conducts a full-service, integrated investment banking, asset management,

and brokerage business. RHBHK

does and seeks to do business with companies covered in its research reports. As a

result, investors should be aware that the firm may have a conflict of interest that

could affect the objectivity of this

research report. Investors should consider this report as only a single factor in making

their investment decision. Importantly, please see the company-specific regulatory

disclosures below for compliance

with specific rules and regulations under the Hong Kong jurisdiction. Other than

company-specific disclosures relating to RHBHK, this research report is based on current

public information that we

consider reliable, but we do not represent it is accurate or complete, and it should not

be relied on as such.

United States

This report was prepared by RHB and is being distributed solely and directly to “major”

U.S. institutional investors as defined under, and pursuant to, the requirements of Rule

15a-6 under the U.S.

Securities and Exchange Act of 1934, as amended (the “Exchange Act”). Accordingly,

access to this report via Bursa Marketplace or any other Electronic Services Provider is

not intended for any party other

than “major” US institutional investors, nor shall be deemed as solicitation by RHB in

any manner. RHB is not registered as a broker-dealer in the United States and does not

offer brokerage services to

U.S. persons. Any order for the purchase or sale of the securities discussed herein that

are listed on Bursa Malaysia Securities Berhad must be placed with and through Auerbach

Grayson (“AG”). Any order

for the purchase or sale of all other securities discussed herein must be placed with

and through such other registered U.S. broker-dealer as appointed by RHB from time to

time as required by the Exchange

Act Rule 15a-6. This report is confidential and not intended for distribution to, or use

by, persons other than the recipient and its employees, agents and advisors, as

applicable. Additionally, where

research is distributed via Electronic Service Provider, the analysts whose names appear

in this report are not registered or qualified as research analysts in the United States

and are not associated

persons of Auerbach Grayson AG or such other registered U.S. broker-dealer as appointed

by RHB from time to time and therefore may not be subject to any applicable restrictions

under Financial Industry

Regulatory Authority (“FINRA”) rules on communications with a subject company, public

appearances and personal trading. Investing in any non-U.S. securities or related

financial instruments discussed in

this research report may present certain risks. The securities of non-U.S. issuers may

not be registered with, or be subject to the regulations of, the U.S. Securities and

Exchange Commission. Information

on non-U.S. securities or related financial instruments may be limited. Foreign

companies may not be subject to audit and reporting standards and regulatory

requirements comparable to those in the United

States. The financial instruments discussed in this report may not be suitable for all

investors. Transactions in foreign markets may be subject to regulations that differ

from or offer less protection

than those in the United States.

RHB Investment Bank Berhad, its subsidiaries (including its regional offices) and associated companies, (“RHBIB Group”) form a diversified financial group, undertaking various investment banking activities which include, amongst others, underwriting, securities trading, market making and corporate finance advisory.

As a result of the same, in the ordinary course of its business, any member of the RHBIB Group, may, from time to time, have business relationships with or hold positions in the securities (including capital market products) or perform and/or solicit investment, advisory or other services from any of the subject company(ies) covered in this research report.

While the RHBIB Group will ensure that there are sufficient information barriers and internal controls in place where necessary, to prevent/manage any conflicts of interest to ensure the independence of this report, investors should also be aware that such conflict of interest may exist in view of the investment banking activities undertaken by the RHBIB Group as mentioned above and should exercise their own judgement before making any investment decisions.

Malaysia

Save as disclosed in the following link (RHB Research conflict disclosures – Jan 2020)

and to the best of our knowledge, RHBIB hereby declares that:

1. RHBIB does not have a financial interest in the securities or other capital market

products of the subject company(ies) covered in this report.

2. RHBIB is not a market maker in the securities or capital market products of the

subject company(ies) covered in this report.

3. None of RHBIB’s staff or associated person serve as a director or board member* of

the subject company(ies) covered in this report

*For the avoidance of doubt, the confirmation is only limited to the staff of research

department

4. Save as disclosed below, RHBIB did not receive compensation for investment banking or

corporate finance services from the subject company in the past 12 months.

5. RHBIB did not receive compensation or benefit (including gift and special cost

arrangement e.g. company/issuer-sponsored and paid trip) in relation to the production

of this report.

Thailand

RHB Securities (Thailand) PCL and/or its directors, officers, associates, connected

parties and/or employees, may have, or have had, interests and/or commitments in the

securities in subject company(ies)

mentioned in this report or any securities related thereto. Further, RHB Securities

(Thailand) PCL may have, or have had, business relationships with the subject

company(ies) mentioned in this report. As

a result, investors should exercise their own judgment carefully before making any

investment decisions.

Indonesia

PT RHB Sekuritas Indonesia is not affiliated with the subject company(ies) covered in

this report both directly or indirectly as per the definitions of affiliation above.

Pursuant to the Capital Market

Law (Law Number 8 Year 1995) and the supporting regulations thereof, what constitutes as

affiliated parties are as follows:

1. Familial relationship due to marriage or blood up to the second degree, both

horizontally or vertically;

2. Affiliation between parties to the employees, Directors or Commissioners of the

parties concerned;

3. Affiliation between 2 companies whereby one or more member of the Board of Directors

or the Commissioners are the same;

4. Affiliation between the Company and the parties, both directly or indirectly,

controlling or being controlled by the Company;

5. Affiliation between 2 companies which are controlled, directly or indirectly, by the

same party; or

6. Affiliation between the Company and the main Shareholders.

PT RHB Sekuritas Indonesia is not an insider as defined in the Capital Market Law and the information contained in this report is not considered as insider information prohibited by law. Insider means:

a. a commissioner, director or employee of an Issuer or Public Company;

b. a substantial shareholder of an Issuer or Public Company;

c. an individual, who because of his position or profession, or because of a business

relationship with an Issuer or Public Company, has access to inside information; and

d. an individual who within the last six months was a Person defined in letters a, b or

c, above.

Singapore

Save as disclosed in the following link (RHB Research conflict disclosures – Jan 2020)

and to the best of our knowledge, RHB Securities Singapore Pte Ltd hereby declares that:

1. RHB Securities Singapore Pte Ltd, its subsidiaries and/or associated companies do not

make a market in any issuer covered in this report.

2. RHB Securities Singapore Pte Ltd, its subsidiaries and/or its associated companies

and its analysts do not have a financial interest (including a shareholding of 1% or

more) in the issuer covered in

this report.

3. RHB Securities, its staff or connected persons do not serve on the board or trustee

positions of the issuer covered in this report.

4. RHB Securities Singapore Pte Ltd, its subsidiaries and/or its associated companies do

not have and have not within the last 12 months had any corporate finance advisory

relationship with the issuer

covered in this report or any other relationship that may create a potential conflict of

interest.

5. RHB Securities Singapore Pte Ltd, or person associated or connected to it do not have

any interest in the acquisition or disposal of, the securities, specified securities

based derivatives contracts or

units in a collective investment scheme covered in this report.

6. RHB Securities Singapore Pte Ltd and its analysts do not receive any compensation or

benefit in connection with the production of this research report or recommendation.

Hong Kong

The following disclosures relate to relationships between RHBHK and companies covered by

Research Department of RHBSHK and referred to in this research report:

RHBSHK hereby certifies that no part of RHBSHK analyst compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this research report.

RHBHK had an investment banking services client relationships during the past 12 months with: -.

RHBHK has received compensation for investment banking services, during the past 12 months from: -.

RHBHK managed/co-managed public offerings, in the past 12 months for: -.

On a principal basis. RHBHK has a position of over 1% market capitalization of: -.

Ownership and material conflicts of interest: RHBSHK policy prohibits its analysts and associates reporting to analysts from owning securities of any company covered by the analyst.

Analyst as officer or director: RHBSHK policy prohibits its analysts, and associates reporting to analysts from serving as an officer, director, advisory board member or employee of any company covered by the analyst.

RHBHK salespeople, traders, and other non-research professionals may provide oral or written market commentary or trading strategies to RHB clients that reflect opinions that are contrary to the opinions expressed in this research report.