It’s dividend time! When the Employees Provident Fund (EPF) announces its annual dividend, we pay very close attention. While 2025’s dividend of 6.15% was slightly lower than 2024’s 6.30%, it’s nothing to turn up our noses at. For most of us, EPF is the largest pool of long-term savings we will accumulate in our lifetime. For some, it’s the only form of sustainable and disciplined savings.

Which brings us to a very important question: Are your EPF savings alone enough to support the retirement lifestyle you envision?

The annual dividend announcement is more than just a financial update. It is also a useful opportunity to reflect on how your retirement strategy is progressing. It forces you to confront the possibility that, maybe, your golden years won’t be as golden as you thought.

Let’s understand how EPF works, so we can use it as part of a broader strategy.

EPF is one of Malaysia’s largest institutional investors. To generate returns for contributors, it invests across a diversified portfolio of assets, including:

- Malaysian and global equities

- Fixed income instruments such as bonds and sukuk

- Real estate and infrastructure investments

- Money market instruments

Each year, the dividend declared by EPF is based on a combination of:

- Investment income earned during the year

- Realised capital gains

- Reserves accumulated from previous years

These earnings are then distributed to contributors in the form of the annual dividend.

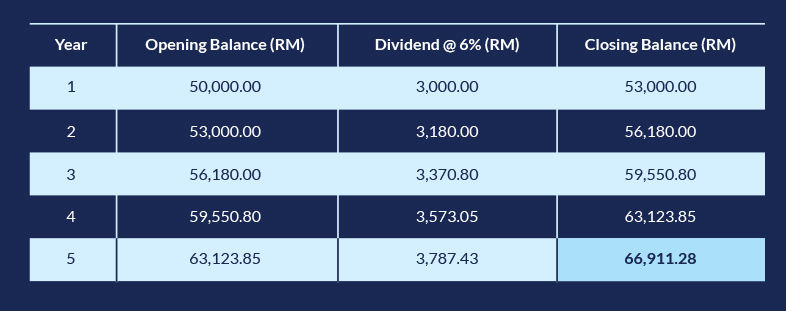

One important feature of EPF is compounding. When dividends are credited into your EPF account, they become part of your principal balance and generate returns in subsequent years. Over time, this compounding effect can significantly increase the value of retirement savings. We’ll use a fixed return of 6% per year and an initial principal of RM50,000 to illustrate the power of compounding:

After 5 years, the RM50,000 grows to approximately RM66,911, even without additional contributions.

Total dividends earned: RM16,911

However, it is important to remember that EPF dividends are not guaranteed. They depend on the performance of the underlying investments and broader economic conditions. You’re not getting 6% a year.

While percentages may sound impressive, it often helps to translate them into actual figures. Here are some simple illustrations based on the latest dividend rate:

For many contributors, this annual dividend represents a meaningful addition to their long-term savings. But again, will your EPF balance at retirement be enough to support you – comfortably – for at least 20 years?

To answer that question, it helps to think about:

- How much income you may require each month in retirement

- How many years your retirement savings need to last

- Whether your current savings trajectory supports those goals

There is good reason why EPF plays such a central role in retirement planning for Malaysians. Its structure offers several important advantages.

First, mandatory contributions encourage long-term savings discipline. Regular monthly contributions ensure that individuals steadily build retirement funds over their working lives. Second, EPF benefits from professional institutional management. With a large and diversified investment portfolio, the fund can access opportunities across global markets. Third, EPF places strong emphasis on capital preservation and stability, helping contributors navigate different economic cycles.

Taken together, these features make EPF a strong foundation for retirement planning. However, like any financial tool, it also has limitations.

While EPF provides an important base for retirement savings, it was designed primarily as a retirement security mechanism, rather than a complete wealth accumulation vehicle. There are several factors contributors should keep in mind.

- Withdrawal restrictions: Access to EPF funds is largely limited until retirement age, which means the savings are not always flexible for other financial goals.

- Dividends may fluctuate over time, depending on market conditions and investment performance.

Inflation also plays a role in determining the real value of returns. If inflation averages around 3% annually, a 6.15% dividend would translate to a real return of approximately 3.15% after accounting for rising living costs. Over time, inflation can reduce the purchasing power of your savings if they do not grow fast enough.

One commonly used rule of thumb in retirement planning is the 240x monthly expenses benchmark. This approach estimates the size of retirement savings needed to sustain a certain lifestyle.

For example:

If your expected retirement expenses are RM8,000 per month, the estimated savings target would be:

RM8,000 × 240 = RM1.92 million

While this is only a general guideline, it provides a useful starting point for assessing retirement readiness.

From there, you may consider questions such as:

- Will my projected EPF balance reach that level?

- What if I plan to retire earlier than expected?

- How might healthcare costs affect my future expenses?

These reflections help shift the conversation from annual dividends to long-term retirement sustainability.

For many individuals, EPF serves as the backbone of retirement planning. At the same time, some investors choose to complement their EPF savings with diversified investment strategies that support broader financial goals.

Examples may include:

- Unit trust portfolios

- Multi-asset investment strategies

- Structured investment solutions

- Shariah-compliant wealth portfolios

- Professionally managed investment plans

These approaches can help individuals pursue goal-based investing, where portfolios are structured around long-term objectives such as retirement income, capital growth, or wealth preservation. Don’t worry, you don’t have to do all the research and math by yourself, but it does help to have a basic understanding of how each of these approaches works. Then, your Relationship Manager can help you build a portfolio that suits your risk appetite and goals.

The EPF dividend itself reflects how global investment markets evolve from year to year. Equity markets, interest/profit rates, and currency movements all influence overall investment performance. Diversification across geographies and asset classes helps manage these fluctuations over time.

For individual investors managing their own portfolios, maintaining disciplined asset allocation and regular portfolio reviews can play an important role in navigating market cycles effectively.

This is where structured financial planning and professional advisory support may help investors remain aligned with their long-term goals.

Retirement strategies often evolve as individuals progress through different stages of life.

Age 25–35

At this stage, the focus is typically on growth and accumulation. Investors may have a longer time horizon, allowing for a higher allocation to growth assets. EPF provides the savings foundation, while additional investments may support wealth accumulation.

Age 35–50

Financial priorities often shift toward balancing growth with capital protection. Diversified portfolios may become increasingly important as responsibilities such as family expenses and housing commitments grow.

Age 50 and above

The focus gradually transitions toward income generation and capital preservation. Retirement planning becomes more concrete, and strategies may shift toward assets designed to support stable income streams.

Ultimately, the EPF dividend announcement is more than just a yearly financial milestone. It serves as a reminder to review whether your overall wealth strategy is aligned with your long-term retirement aspirations.

While EPF remains a powerful pillar of retirement security for Malaysians, taking a broader view of financial planning can help ensure that your savings continue to support the lifestyle you envision in the years ahead. Reviewing your retirement strategy periodically, whether independently or with a qualified financial adviser, can help keep your financial plans on track as circumstances evolve.

Investors are advised to read and understand content of the relevant documents including but not limited to prospectus or information memorandum that has been registered with Securities Commission and Product Highlight Sheet before investing. Investors should also consider all fees and charges involved before investing. Prices of units and income distribution, if any, may go down as well as up; where past performance is no guarantee of future performance. Units will be issued upon receipt of the registration form referred to and accompanying the Prospectus. The printed copy of prospectus and ProductHighlight Sheet is available at RHB branches/Premier Centre and investors have the right to request for a Product Highlight Sheet.

This article has not been reviewed by the Securities Commission Malaysia (SC).

RHB Bank Berhad 196501000373 (6171-M) | RHB Islamic Bank Berhad 200501003283 (680329-V)